The 60-Second Version

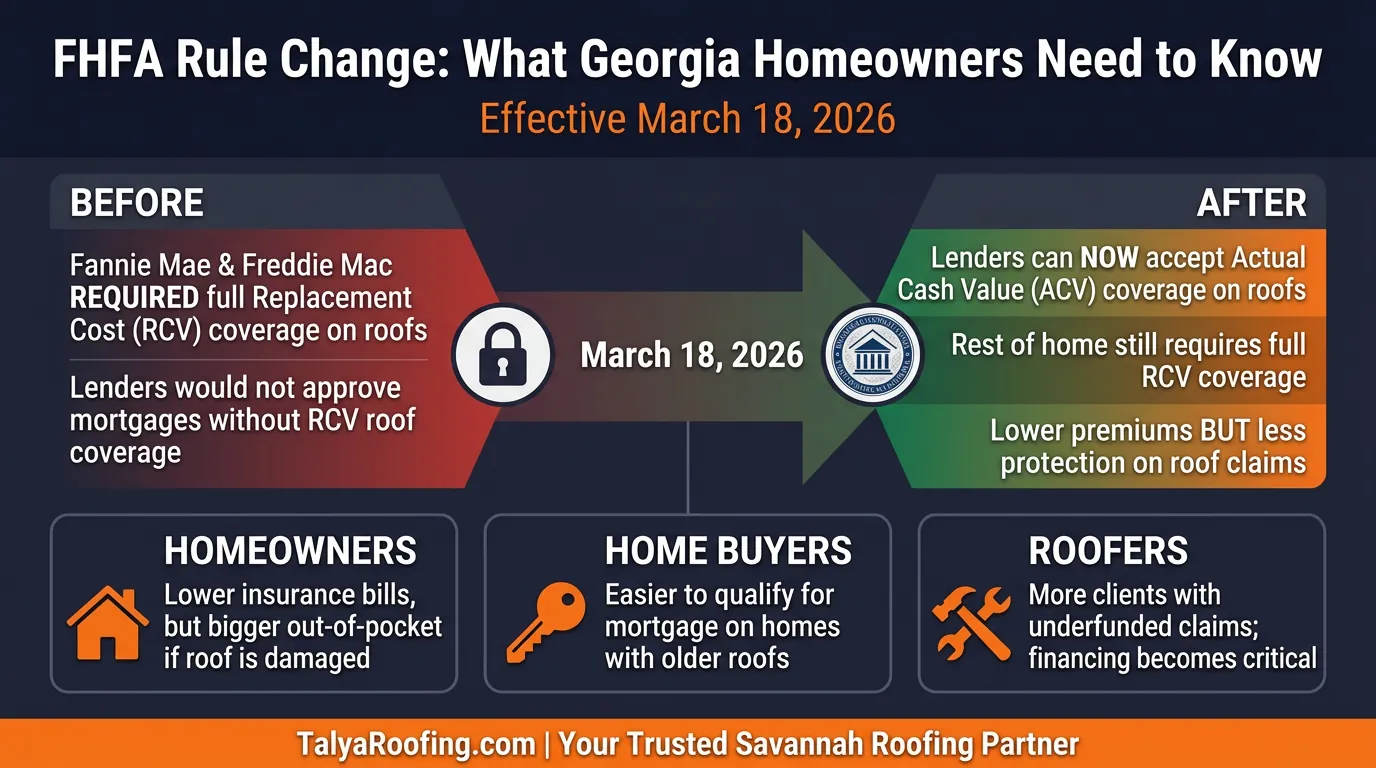

- What happened: On March 18, 2026, the FHFA told Fannie Mae and Freddie Mac they can now accept roof insurance policies that pay Actual Cash Value (ACV) instead of full Replacement Cost Value (RCV).

- Why it matters: About 70% of conventional mortgages are Fannie/Freddie-backed. Millions of homeowners will likely switch to cheaper ACV roof coverage—or their insurer will switch them.

- The trade-off: Lower monthly premiums now, but dramatically less money from insurance if a storm damages your roof. The older your roof, the bigger the gap you pay out of pocket.

- What to do: Check your policy, understand your coverage type, and know your options before storm season. Contact Talya Roofing for a free roof inspection and honest assessment.

What the FHFA Rule Change Actually Did

On March 18, 2026, the Federal Housing Finance Agency (FHFA) announced one of the most significant changes to homeowners insurance requirements in over a decade. Here is what changed:

- Before March 2026: Fannie Mae and Freddie Mac required homeowners with their mortgages to carry Replacement Cost Value (RCV) coverage on their roofs. If your policy only covered the roof at Actual Cash Value, your lender could force-place more expensive coverage or refuse to process your loan.

- After March 2026: Lenders selling loans to Fannie Mae and Freddie Mac can now accept Actual Cash Value (ACV) coverage on the roof portion of homeowners policies. The rest of the house still requires full RCV coverage.

- Additional changes: The FHFA also simplified deductible rules for condos, expanded eligibility for condo projects, and rescinded a controversial 2024 policy clarification that had slowed insurance claims.

This change applies to new mortgages and renewals on loans Fannie Mae and Freddie Mac purchase or guarantee—which represents roughly 70% of all conventional mortgages in the United States. That makes this the broadest change to mortgage-related insurance requirements in years.

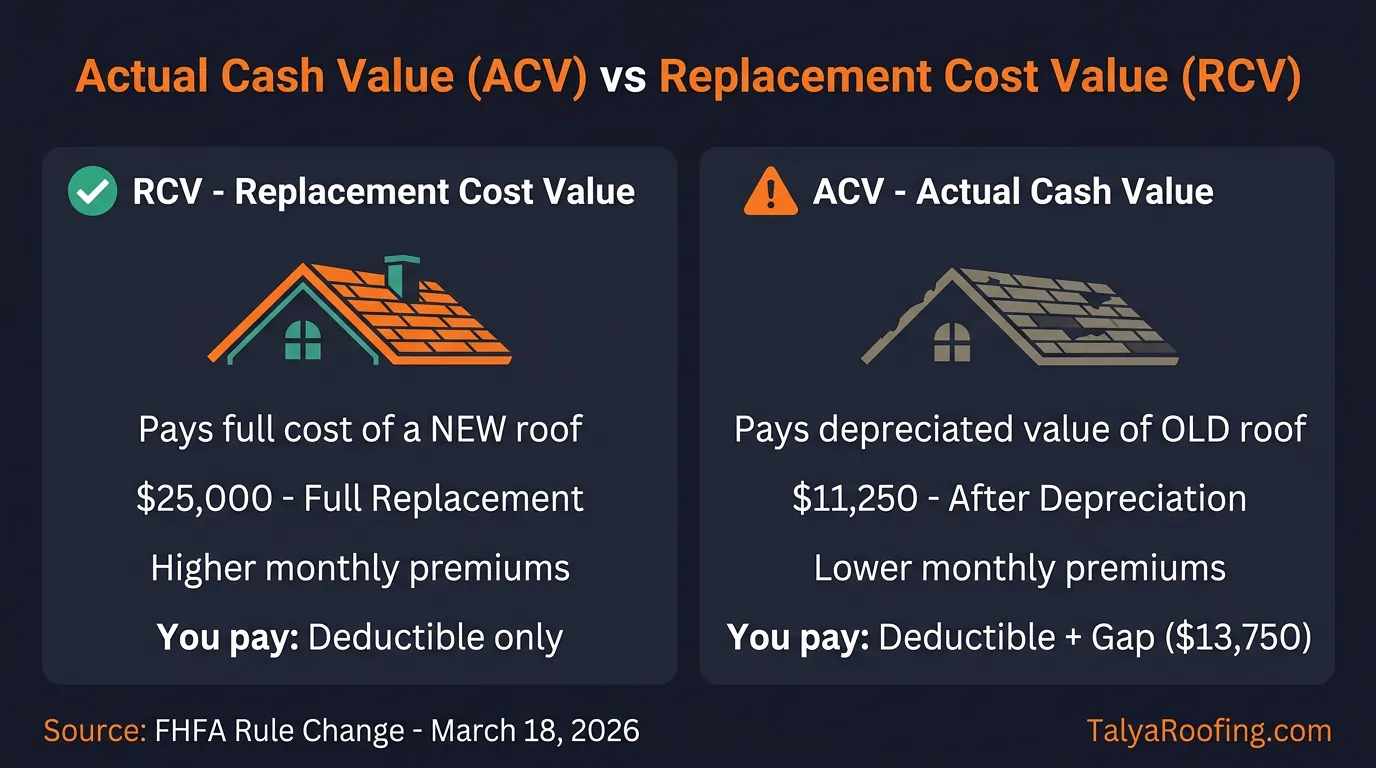

ACV vs RCV: The Two Types of Roof Insurance Explained

This is the single most important concept in this entire article. Understanding the difference between Actual Cash Value and Replacement Cost Value will determine whether you are prepared or blindsided when a storm hits your roof.

| Feature | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| What it pays | Full cost of a brand-new roof of similar quality | Current depreciated value of your existing roof |

| Depreciation applied? | No — age does not reduce payout | Yes — payout shrinks every year as roof ages |

| Monthly premium | Higher | Lower |

| Out-of-pocket after a claim | Deductible only | Deductible + depreciation gap |

| Best for | Maximum protection; peace of mind | Lower monthly costs; newer roofs |

| Roof age risk | Low — payout is the same whether roof is 2 or 22 years old | High — payout drops dramatically as roof ages |

Think of it this way: RCV insures your roof like a new car—if it gets totaled, you get a new one. ACV insures your roof like a used car—if it gets totaled, you get a check for what the old one was worth, and you are responsible for the difference if you want a new one.

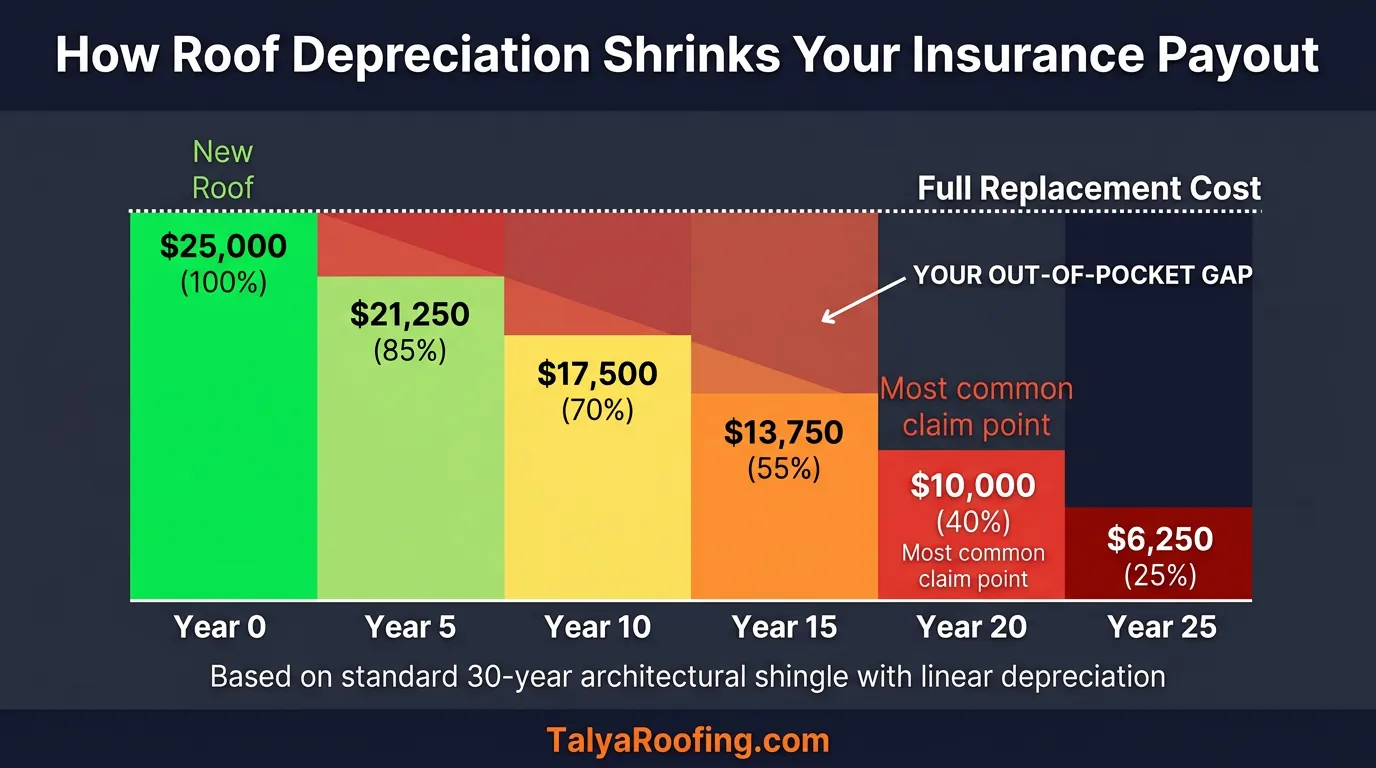

How Depreciation Works on Your Roof

Insurance companies calculate roof depreciation using a formula that accounts for the roof's age, expected lifespan, and condition. For a standard 30-year architectural shingle roof (the most common type in Savannah and Coastal Georgia), depreciation is typically calculated on a linear basis.

Here is what that looks like in real dollars on a $25,000 roof replacement:

| Roof Age | Value Remaining | ACV Payout | Your Out-of-Pocket Gap |

|---|---|---|---|

| Brand New | 100% | $25,000 | $0 |

| 5 years | 83% | $20,750 | $4,250 |

| 10 years | 67% | $16,750 | $8,250 |

| 15 years | 50% | $12,500 | $12,500 |

| 18 years | 40% | $10,000 | $15,000 |

| 20 years | 33% | $8,250 | $16,750 |

| 25 years | 17% | $4,250 | $20,750 |

Key takeaway: By year 15, your ACV payout only covers half the cost of a new roof. By year 20—when most Savannah roofs start showing real storm damage—you are looking at paying $16,750+ in depreciation alone on top of your deductible just to get back to a proper, warrantied roof. With RCV coverage, you would pay only your deductible regardless of roof age.

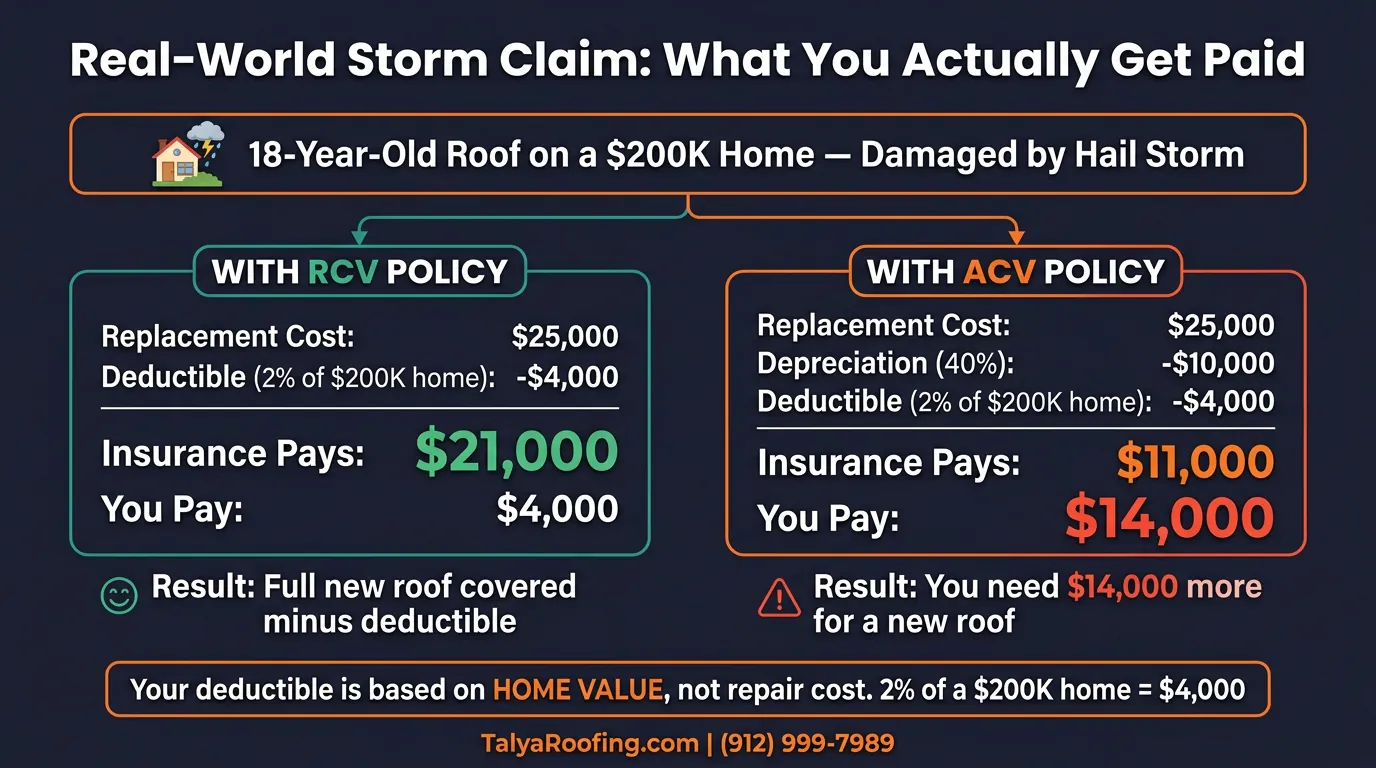

Real-World Storm Claim: ACV vs RCV Payout

Let us walk through a scenario that Georgia homeowners face regularly. A hailstorm hits Savannah and damages the roof on a $200,000 home that is 18 years old. The full cost to replace the roof is $25,000. The homeowner has a standard 2% deductible—which is calculated on the home's insured value, not the roof cost. On a $200K home, that is a $4,000 deductible.

With RCV Policy

- Replacement Cost: $25,000

- Deductible (2% of $200K home): -$4,000

- Insurance Pays: $21,000

- You Pay: $4,000

Full new roof covered minus your deductible.

With ACV Policy

- Replacement Cost: $25,000

- Depreciation (40%): -$10,000

- Deductible (2% of $200K home): -$4,000

- Insurance Pays: $11,000

- You Pay: $14,000

You need $14,000 more for a full new roof.

How the deductible works: Your deductible percentage is applied to your home's total insured value—not the cost of the repair. A 2% deductible on a $200,000 home is $4,000. On a $300,000 home, it is $6,000. On a $400,000 home, it is $8,000. This is true whether the damage is a $5,000 repair or a $25,000 full replacement.

That $14,000 difference is not hypothetical. It is the exact gap that thousands of Georgia homeowners will face after the next major storm event. And with this FHFA rule change, more mortgage holders than ever will be carrying ACV-only roof coverage when that storm arrives.

Why Premiums Are Dropping — But Protection Is Too

The FHFA rule change is being driven by a real affordability crisis. Here are the numbers:

- 46% premium increase since 2021 — average homeowners insurance costs have skyrocketed nationwide

- $2,948 average annual premium by end of 2025 — a significant and unwelcome addition to monthly housing costs

- 70% of conventional mortgages are Fannie/Freddie-backed — this change touches the vast majority of homeowners

- In many states, full RCV roof coverage has become extremely expensive or simply unavailable for homes with roofs older than 10–15 years

- More than 45 members of Congress signed letters urging FHFA to make this change, calling the old requirement “big government overreach”

The logic from a policy perspective is straightforward: if millions of families cannot afford insurance that meets the old federal standard, make the standard more flexible. Lower insurance costs also reduce monthly mortgage payments, which helps first-time homebuyers qualify for loans they otherwise could not afford.

But from a homeowner protection perspective, the math goes the other way. You are trading lower monthly costs today for the risk of a five-figure bill when the next storm hits. The premium savings over 10 years might total $3,000–$5,000. A single ACV claim gap on a 15-year-old roof could cost you $12,500 in depreciation—plus your deductible on top of that.

The uncomfortable truth: Insurance premiums went down, but so did the safety net. You are not saving money — you are shifting risk from your insurance company to yourself.

What This Means for Georgia Homeowners

Georgia is already one of the hardest-hit states when it comes to roof insurance changes. Here is what makes our market especially vulnerable:

- Georgia insurers were already pushing ACV: Before this federal change, many Georgia carriers had been moving toward ACV roof endorsements because of rising storm and reinsurance costs. The FHFA change removes the last major barrier that was keeping some policies at RCV.

- Active storm corridor: Savannah and Coastal Georgia sit in one of the most active weather corridors in the Southeast for hail and wind events. We get storms. Roofs get damaged. Claims happen.

- Aging housing stock: Many homes in Savannah, Pooler, Richmond Hill, and the surrounding areas have roofs that are 15–25 years old — right in the range where ACV depreciation creates the biggest out-of-pocket gap.

- Georgia's Act 277 (Senate Bill 35): effective January 1, 2026, it extends the homeowners-insurance non-renewal notice period from 30 to 60 days. Combined with this FHFA change, the insurance landscape for Georgia roofs is shifting faster than most homeowners realize. (Read more: Georgia Roof Insurance Act 277 Explained)

The combination of state-level insurance changes, rising costs, and this new federal flexibility creates a situation where tens of thousands of Coastal Georgia homeowners could be sitting on policies that will not fund a full roof replacement when the next storm hits.

What This Means If You Are Buying a Home

For homebuyers, this FHFA change is a double-edged sword:

The Good News

- Easier to qualify for a mortgage on homes with older roofs

- Lower insurance premiums reduce your total monthly payment

- Fewer deals killed by insurance requirements

- More flexibility in choosing your coverage level

The Risk

- You may be buying with less roof protection than you realize

- The roof you are inheriting may already be past the point where ACV provides meaningful coverage

- A roof replacement could cost $15,000+ out of pocket if a storm hits within the first few years

- Factor potential roof costs into your purchase budget — not just the mortgage payment

Our advice for buyers: Before closing, get a professional roof inspection that tells you the roof's exact age, condition, estimated remaining life, and approximate replacement cost. Then check whether the homeowners policy you are being offered is ACV or RCV on the roof. If it is ACV and the roof is already 12+ years old, factor $10,000–$20,000 in potential out-of-pocket roof costs into your financial planning. Schedule a free inspection with Talya Roofing before you close.

The Georgia Factor: Why This Hits Our Market Harder

Not every state will feel this change equally. Here is why Coastal Georgia homeowners should pay especially close attention:

| Factor | Georgia Reality | Impact on ACV Claims |

|---|---|---|

| Storm frequency | 2–4 significant hail/wind events per year in Savannah area | High claim probability |

| Average roof age | 15–20 years for much of the existing housing stock | Maximum depreciation zone |

| Humidity and salt air | Accelerates shingle degradation beyond normal wear | Adjusters may depreciate faster |

| Replacement costs | $18,000–$28,000 for typical Savannah home | Large dollar gaps on older roofs |

| Insurer behavior | GA carriers already aggressive on ACV endorsements | More policies will shift to ACV |

Your 3 Options When ACV Leaves You Short

If a storm damages your roof and your ACV payout does not cover a full replacement, you are not stuck. Here are the three paths we walk homeowners through every week:

Option 1: ACV Check + Financing = Full New Roof (Most Popular)

Use your insurance payout as a down payment and finance the remaining gap with low monthly payments. This is the most common approach we see, and it gets you a full, warrantied replacement without draining your savings. Learn about our financing options.

Option 2: Partial Repair (Insurance Check Only)

Use your ACV check for targeted repairs to the damaged sections. This can extend your roof's functional life by 3–5 years. It is the best option for tight budgets, but understand it is a short-term fix — not a long-term solution. The underlying aging issue remains.

Option 3: Full Replacement (Check + Cash)

Combine your ACV payout with savings to fund the full replacement out of pocket. No financing costs, no interest. This gives you the best long-term value if you have the cash available.

How Talya Roofing Helps You Navigate ACV Claims

We work with homeowners on insurance-related roof projects every week. Here is exactly how we help when you are dealing with an ACV claim:

- Free professional inspection: We document every inch of your roof with photos, measurements, and condition notes. This gives you a clear picture of what needs to happen — not what your insurance company says needs to happen.

- Transparent pricing: We provide a detailed, line-item estimate for both a full replacement and a targeted repair. No hidden costs. No surprises. You see exactly what things cost.

- ACV gap analysis: We compare your insurance payout to our estimate and show you the exact dollar gap. Then we walk you through your three options so you can make an informed decision.

- Financing coordination: If you choose Option 1 (ACV check + financing), we help coordinate the process so it is seamless. Most homeowners qualify for $0-down financing with payments starting after the work is complete.

- Quality installation: Whether it is a full replacement or a targeted repair, every job gets the same attention to detail. Atlas Pro+ certified. 130 MPH wind-rated. Built for Coastal Georgia.

We do not adjust claims. We do not give insurance advice. What we do is give you the honest information you need to make the best decision for your home and your family. Schedule your free inspection today or call us at (912) 999-7989.

5 Things Every Homeowner Should Do Right Now

Check your policy

Call your insurance agent and ask one question: “Is my roof covered at Replacement Cost or Actual Cash Value?” If they say ACV, ask what your depreciation percentage would be based on your roof's current age.

Know your roof's age

If you do not know when your roof was last replaced, check your closing documents, ask a neighbor who built around the same time, or have a roofer estimate it during an inspection.

Get a professional inspection

A qualified roofer can tell you your roof's current condition, estimated remaining life, and approximate replacement cost. This information is critical for understanding your actual financial exposure.

Do the math on RCV vs ACV

Compare the premium savings of ACV against your potential out-of-pocket exposure. If keeping RCV only costs an extra $300–$600 per year and your roof is 12+ years old, that premium difference is almost certainly worth paying.

Have a plan before storm season

Do not wait until a storm hits to figure out what your policy covers. Know your coverage type, your estimated gap, and your financing options now so you can make a clear-headed decision when the time comes.

New Georgia Laws That Affect Your Roof Insurance in 2026

The FHFA rule change is not the only major shift for Georgia homeowners in 2026. The Georgia General Assembly passed two important bills, and a new cancellation notice rule took effect — all of which directly impact how you insure and repair your roof.

🏛️ HB 423 — No More Deductible Rebates from Contractors

Georgia House Bill 423 makes it explicitly illegal for any roofing contractor to advertise, promise, or provide a rebate on any portion of your insurance deductible. This includes:

- Offering to “cover your deductible” or “waive your out-of-pocket cost”

- Granting discounts tied to insurance claim work

- Providing referral fees, gift cards, or sign-display credits as incentives

Why this matters: If your deductible is $2,500, you must pay that amount yourself. Any contractor offering to absorb it is committing insurance fraud under Georgia statute. This law targets storm-chaser contractors who follow severe weather into Coastal Georgia, offer “free” roofs by waiving deductibles, and deliver substandard work.

🚨 Red flag: If a contractor offers to pay your deductible, report them to the Georgia Insurance Commissioner at 1-800-656-2298. At Talya Roofing, we have never offered deductible rebates because our Atlas Pro+ certified workmanship speaks for itself.

💰 HB 511 — Tax-Free Catastrophe Savings Accounts

Georgia's HB 511 creates Catastrophe Savings Accounts (CSAs) — tax-free accounts specifically for disaster-related expenses like roof repairs, storm damage recovery, and insurance deductible payments.

| Scenario | Without CSA | With CSA |

|---|---|---|

| Annual savings | $0 earmarked | $2,000/yr tax-deductible |

| After 3 years | $0 dedicated | $6,000+ (with tax-free interest) |

| Storm hits — $2,500 deductible | Credit card or scramble | Pay from CSA, no debt |

| ACV gap ($14,000) | Emergency loan | CSA covers partial gap |

| GA tax savings (5.75%) | $0 | ~$115/year |

For Savannah homeowners with ACV roof coverage, a CSA is especially important — it helps bridge the gap between what insurance pays and what your roof actually costs to replace.

📋 60-Day Cancellation Notice Rule

Starting in 2026, Georgia insurance companies must provide at least 60 days notice before canceling or refusing to renew your homeowner insurance policy — doubled from the previous 30-day requirement.

This gives you twice as much time to:

- Shop for alternative coverage from other carriers

- Schedule a roof replacement to satisfy your insurer's requirements

- Get a professional inspection to document your roof's actual condition

- File a complaint with the Georgia Insurance Commissioner if the non-renewal seems unjust

🛡️ FORTIFIED Roof Discounts — Save 5–35% on Premiums

Under new Georgia legislation, insurers are now required to offer premium discounts for homes with IBHS FORTIFIED certified roofs. These discounts range from 5% to 35% depending on certification level.

| FORTIFIED Feature | What It Does | Added Cost |

|---|---|---|

| Sealed roof deck | Prevents water intrusion if shingles blow off | $400–$800 |

| Hurricane clips (roof-to-wall) | Prevents roof from lifting in high winds | $300–$500 |

| Impact-resistant shingles (Class 4) | Resists hail damage up to 2” diameter | $500–$1,200 |

| Drip edge & flashing upgrades | Prevents wind-driven rain at roof edges | $200–$400 |

The ROI: Total FORTIFIED upgrade during a roof replacement: approximately $1,200–$1,800. On a $3,000/year insurance policy with a 15% discount, you save $450/year — the upgrade pays for itself in 3–4 years. FORTIFIED homes also suffer 44% fewer claims (IBHS data).

Sources: IBHS FORTIFIED Home • Georgia 2026 Law Changes • HB 423 Analysis

The Bottom Line

The March 2026 FHFA rule change — combined with Georgia's new HB 423, HB 511, and the 60-day cancellation notice rule — represents the biggest shift in how Georgia homeowners insure their roofs in over a decade. Lower premiums are real — but so is the reduced protection. For Coastal Georgia homeowners, where storms are frequent and roofing costs are substantial, these changes demand attention.

The homeowners who come out ahead will be the ones who:

- Understand exactly what coverage they have

- Know their roof's age and condition

- Have calculated their potential out-of-pocket exposure

- Have a plan (financing, savings, or both) to cover the gap if a storm hits

At Talya Roofing, we believe informed homeowners make the best decisions. That is why we wrote this guide — and why we offer free, no-pressure roof inspections to every homeowner in the Savannah area. Whether you need a full replacement today or just want to understand where you stand, we are here to help.

Get Your Free Roof Inspection

Know your roof's age, condition, and replacement cost before storm season. No pressure, no sales pitch — just honest information.

Schedule Free InspectionOr call (912) 999-7989

Sources: FHFA Press Release (March 18, 2026) • ABA Banking Journal • Ohio Insurance Agents Association • Florida Realtors • John Cobain Home Loans • Davidson Insurance

Disclaimer: This article is for informational purposes only and does not constitute insurance or legal advice. Coverage details vary by policy and insurer. Consult your insurance agent for guidance specific to your situation.